Guest blog from CTVC:

CTVC is the industry leading newsletter powered by Sightline Climate. Their data-driven perspectives power 60,000 investors and operators to innovate on climate. Reach out to hello@ctvc.co

Insurance, the icing on the capital stack cake

The key to unlocking the climate capital stack

As climate tech becomes more fully baked, the layers of the Climate Capital Stack are also sophisticating to meet the requirements for scale – stacking VC rounds on top of government grants, then piling on growth, debt, or project finance. If the layers of the climate capital stack cake are asset classes, the icing on the cake is sweet sweet insurance.

Scaling climate tech requires building infrastructure, and lots of it. One look at all the traditional infra scale-up plays – O&G, the grid, renewables – and it’s clear that almost all of it was deployed with project finance. But “there is no long-term market for project-level financing without insurance,” as Aaron Ratner, Chairman and a Co-founder of CC Risk Solutions, a specialty insurance brokerage focused on renewables, puts it. Without insurance in place, commercial banks won’t lend to, and project finance funds won’t invest in, sustainable infrastructure projects – which means no financing, and no projects.

Insurance can help bridge the gap to bankability by de-risking key ‘bankability blocks’. It acts as a risk transfer mechanism to move risk away from the capital markets into the insurance markets.

Bankability checklist 101

Here are a few highlights of what makes a project “bankable”, pulled from our longer bankability checklist. To meet these necessary conditions, there are key underlying risks that must be mitigated.

- Supply chain: Supply chain for inputs (e.g. feedstocks for RNG or hydrogen production) available at volumes necessary for production.

- Performance: Force majeure, natural catastrophe events, or defects that might impact ability to deliver.

- Reliability of counterparties: Creditworthy customers, suppliers, and contractors with a strong track record of fulfilling obligations.

If these risks are the bankability blocks, think of insurance as the key to unlocking them and paving the way for financing from lenders to come in. Or, put another way – it’s the icing that glues the layer of project finance and debt on to the climate capital cake.

The climate insurance umbrella

Before jumping off the deep end and into the wonky world of insurance, we should note that the term ‘climate insurance’ functions as an umbrella, encompassing all the areas where climate and risk transfer might intersect.

The different types of climate insuretech can be thought of in concentric circles. In the inner circle, there are companies providing insurance to support the transition to a low-carbon economy (we’ll focus here for now). The middle circle is composed of insurance quantifying risk caused by climate change affecting a physical hazard on the ground – think wildfires like Kettle or floods like Delos. Then there’s an even wider layer of parametric insurance, including those offered by Arbol, Descartes, and Demex, which pays out a predetermined amount based on specific events, often in the case of natural disasters or extreme weather.

In this feature, we’ll focus on the inner circle – insurance as a key to unlocking financing for building the new climate economy.

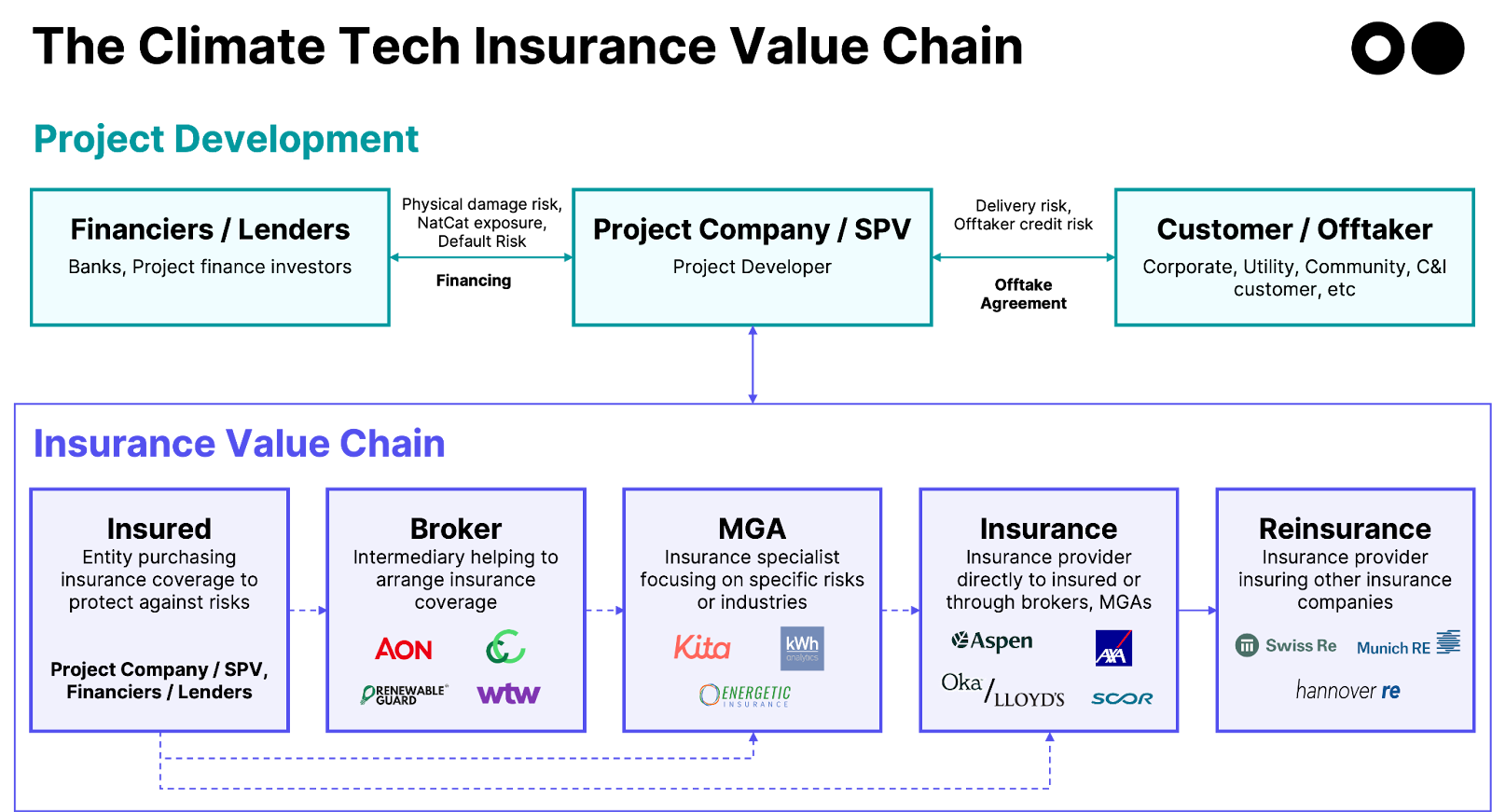

Unlocking the insurance value chain & definitions

First, let’s recap the project development structure and how the insurance value chain fits in.

A simplified view of project development consists of the project company, or a special purpose vehicle (SPV) set up by the developer, the financiers providing them with capital (e.g. project finance investors, banks), and the customers or offtakers purchasing the output (e.g. corporates, utilities).

The financiers (mostly banks) always negotiate insurance as part of their financing terms to protect against key bankability risks. Project developers or lenders then purchase insurance coverage, which is supported by a whole value chain of key players working to transfer those risks from the capital markets to the insurance markets.

- Insured: The individual or entity purchasing insurance coverage to protect against specific risks

- Ex) Independent Power Producers (IPPs), Solar Developers, Carbon Project Developers, Financiers (e.g. banks)

- Broker: Acts as an intermediary, assisting clients in finding and arranging suitable insurance coverage

- Ex) Aon, Climate Commodities, Renewable Guard, WTW

- Managing General Agent (MGA): Specializes in underwriting insurance policies and often focuses on specialized types of risks or industries

- Ex) Kita, Energetic, kWh Analytics

- Insurance Company: Provides insurance policies to the insured through brokers and MGAs, assuming the financial risk

- Ex) Aspen, AXA, Scor, Oka / Lloyd’s

- Reinsurance Company: Offers insurance to insurance companies, helping them manage risk by providing financial protection against large claims

- Ex) Munich Re, Swiss Re, Hannover Re

The insurance specialists

Insurance companies are in the business of risk, but ironically they can be rather risk-averse when it comes to new markets or products, or may simply not have the expertise to underwrite specialized risks. Managing General Agents (MGAs) are insurance providers who have the specialty expertise to design products that better fit new or unique markets that traditional insurance might not cover, or have data and a unique underwriting view on a challenging market (which renewable energy falls into today). They have a symbiotic relationship with large insurers, with MGAs providing the special know-how, backed by insurance companies with large balance sheets.

MGA models in climate tech

Specialty MGAs led by industry experts have been on the rise to tackle different types of risks across climate tech sectors.

- Renewables: Provide credit enhancement to enable debt for projects with sub-IG offtake (Energetic) or focus on underwriting mandatory insurance required by the banks – such as property insurance (kWh Analytics)

- Carbon Markets: Protect buyers / investors against under-delivery or reversal risk of carbon credits (Oka*, Kita) *Oka is a full stack carrier as a LLoyd’s syndicate

- EVs: Enable low-cost leases for low FICO and fleet borrowers (Qover)

We sat down with Energetic, kWh Analytics, Kita, and Oka to understand how their insurance offerings can unlock financing and enable offtake in renewables and carbon markets.

What are the project finance or execution risks?

Jeff McAulay, Nathan Maggiotto @Energetic: One of the key pillars in project finance is a bankable offtaker. ‘Bankable’ basically means credit risk. We think that repayment of electricity is fundamentally different and lower risk than traditional credit metrics suggest. Electricity is essential and payments often survive bankruptcies, even during restructuring. We apply that philosophy in our underwriting to take on what is perceived as credit risk, but we see as a different type of non-payment risk.

Jason Kaminsky @kWh Analytics: Project finance 101 is that you allocate risk to the party who can best handle it. This means the party that can best price and manage the risk. With projects, risk management starts between a client and their bank, but there are a lot of risks. There’s physical damage risk, offtake risk, resource risk, and technology risk. The question and the hurdle becomes, are any of those insurable? For something like physical damage, it’s actually not a risk a bank is willing to take, so you need to find an insurance counterparty. So for any of these risks, can you pay someone to take that risk for you at a reasonable price and be another layer of the value stack?

Natalia Dorfman @Kita: Risk profiles differ depending on the type of carbon project. Nature-based projects like forestry have more familiarity for some investors, for example due to wider timber investment portfolios. However, they might have concerns regarding political, counterparty, and climate risks—particularly in areas prone to natural disasters. Engineered carbon removal projects are more capex-heavy and face technology and scale-up risks, but once up and running can offer investors a risk profile that feels familiar in terms of other infrastructure assets. The major hurdle across all forms of carbon removal projects is that there isn’t enough financing coming in. It’s a chicken and egg situation – all projects will be high risk until they hit key milestones – but insurance can act as the unlock to provide the risk protection to enable financing to help scale high quality projects.

Chris Slater @Oka: When you start a project, from day one to its end, there’s always uncertainty whether it’ll kick off as planned and actually start sequestering carbon. It’s not just about getting it off the ground; even after we issue credits, there’s this ongoing challenge to make sure they keep their value and do their part in meeting net zero goals. Insurance becomes essential across the board, so we’re juggling risks throughout the project lifecycle like reputation, finance, and staying on top of regulations.

How does your insurance mitigate key risks?

Energetic: We isolate and insure one of the few perils that is not backstopped by an existing path to recovery. If your project fails because it was destroyed by a storm and you default on your loan, the bank can recover from the property policy. If your project fails because your panels are defective, there is likely a warranty. If your project fails because your offtaker defaults, what do you do? We developed a novel credit insurance policy that backstops an offtakers ability to make payments under a PPA. This gives project lenders comfort that their loan will be repaid. Instead of relying on payment by an unrated or sub-investment grade counterparty, they can underwrite the rating of the insurer.

kWh Analytics: Our company’s focus these days is on property insurance because it’s proven to be such a big hurdle in today’s market. We built out a data set of the US market, including location, technology and prior loss history. Based on this data, we can model out the probability that an event will happen, and then how that will affect the asset itself. There’s not a lot of information about how solar assets react to different perils so we use our data and actual losses to refine these models and come up with more accurate pricing.

Kita: We focus on delivery risk, protecting buyers and investors of carbon credits against underperformance of the underlying carbon project. Carbon projects forecast their future ability to sequester carbon dioxide, resulting in expected numbers of carbon credits. , However given the long timeframes of carbon projects, there’s risk that these carbon credits might not be delivered – for example due to natural catastrophe, counterparty risk, changes to carbon methodologies, or political and regulatory risk. Early-stage projects need investments to scale, and insurance provides the security needed to unlock financing at scale.

Oka: We cover two main buckets: invalidation and reversal risk. If carbon gets put back into the atmosphere by virtue of either a natural catastrophe, or by something human induced like illegal logging, you risk invalidation of credits. In any one of those situations, if the registry chooses to invalidate or remove the credit, then our policy pays out. So we price for all these coverages against many carbon project types.

Who do you sell to within this insurance value chain?

Energetic: Our customer is the project developer, but we work closely with banks as they are often the beneficiary. Our insurance policy is purchased to achieve a KPI; that may be turning a “no” into a “yes”; or it may be giving the lender added comfort in exchange for optimal financing terms.

kWh Analytics: In this value chain, who you de-risk is who your customer is, so we cover the developer, primarily in solar and storage.

Kita: We primarily work with experienced intermediaries such as the financier/lender, asset manager, or broker who are investing in early-stage carbon projects and see insurance as an enabler to reduce risk and improve capital efficiency. We also work with corporates who want increased security on their purchases and we’re developing insurance for project developers as well.

Oka: We target the post-issuance stage of credits, similar to how bonds work. We wrap these issued credits with our insurance product, making them more appealing in the market. It’s like giving the credit a quality boost and a safety net for the buyers. We get in there at the point of sale through intermediaries so when companies like South Pole or Climate Impact Partners are dealing with their clients, our insured credit could be embedded as part of the overall package.

MGA vs. general insurer, clarify the advantages?

Energetic: Insurers work through MGAs for two reasons: specialized domain expertise and unique market access. We are energy project specialists tapped into a market that our insurer would not otherwise see risks in. We enable an insurer to extend their footprint, while relying our specialized expertise to do so.

kWh Analytics: MGAs know that specialty risk and can help to underwrite and access it. In order to do it well, you need specialty knowledge, which large scale insurance companies just don’t have. It’s the same with knowledge of the local markets. We offer a unique product that others might not know how to structure, as the only insurance underwriters who come from the renewables industry.

Kita: Insurance is meant to cover risk, but as an industry overall it’s relatively risk averse, particularly for new markets where there isn’t historical data to price the risk. Specialized MGAs focus on understanding, pricing and structuring these emerging and evolving risks, providing a more cost-effective route for larger insurers to access new insurance markets.

Oka: Large carriers struggle because they want 40 years of auditable data to be able to assess the claims history and price the risk accordingly. What we need to be able to do is differentiate between a good versus bad project. So we use data, price it, and then get into the market to test it and iterate from there.

What’s your diligence process for underwriting risk?

Energetic: We quantify the gap between perceived and actual risk. We take a view on credit risk and then layer in a view on the price of electricity, the health of the regional real-estate market, and historical loss data.

kWh Analytics: For property insurance, we take a very technical view and model each location through a natural catastrophe model to determine the probability of loss, adjusting the loss forecasts based on our proprietary data. We give feedback to our clients on resiliency measures that would improve their risk profile.

Kita: We look at a wide spread of risk factors, from political and regulatory risks, to project developer track record, creditworthiness, and contract terms, alongside natural catastrophe and business interruption risks. We get data from public registries, ratings and data providers, and also use proxy data and proprietary data we access from the projects we see. We do extensive due diligence and only insure projects we truly think meet all the quality criteria in the carbon markets, hopefully providing a stamp of confidence for our clients.

Oka: We’ve built our pricing underwriting models over the last 9-10 months and have priced about 7,000 projects. We insure nature based technology engineered removals and removals in all regions or locations. We’ve taken an underwriting approach to it but we’re effectively now working with customers to embed it into their point of sale of all carbon credits.

How does your insurance product “unlock” financing?

Energetic: We helped a bank execute financing for a regional electricity cooperative that was not publicly rated, adding over 20 MW of clean energy supply for the co-ops customers. In another example, we helped a large C&I developer secure flexible financing for a portfolio that included sub-investment grade and unrated counterparties on investment grade terms.

kWh Analytics: Using our Solar Revenue Put insurance, we were able to protect a utility scale solar project in Texas, guaranteeing production for the next 10 years. Three years later there were major production losses due to Winter Storm Uri, but since they had our insurance product they were insulated from any major financial losses that would’ve been associated with it.

Kita: We just announced an MOU with PYREG, which is launching PYREG Climate Finance Solutions (PCFS), a first-of-its-kind leasing scheme targeting to deploy carbonization systems for 150 biochar projects by 2040. PCFS will finance their machines through pre-purchases of biochar carbon removal credits and lease their machines to agricultural businesses producing the biochar. Kita’s insurance product, Carbon Purchase Protection Cover, will be implemented as part of the PCFS facility and provides a protective wrap which protects against under-delivery and provides the stamp of confidence for prospective credit buyers.

Starting to get a sweet tooth for insurance? Folks across the renewables and carbon project development stack (developers, buyers, investors / financiers, etc.) should get in touch with Energetic, kWh Analytics, Kita, and Oka.

A note from Insurtech Gateway

“A big thank you to CTVC for shining a light on the sweet sweet icing of insurance and for allowing us to share your blog. You can see the original here. At Insurtech Gateway we are eager to support founders using insurance to help bridge the gap to bankability. So if you are building a risk transfer mechanism to move risk away from the capital markets into the insurance markets, please get in touch.”